Transition from Structural Reforms

to a Full‑Fledged

Growth Strategy

Boost 2028

Accelerating

Strong Sumitomo Pharma

SCROLL

Disclaimer Regarding Forward-looking Statements

- This material contains forecasts, projections, goals, plans, and other forward-looking statements regarding the Group’s financial results and other data. Such forward-looking statements are based on the Company’s assumptions, estimates, outlook, and other judgments made in light of information available at the time of disclosure of such statements and involve both known and unknown risks and uncertainties.

- Accordingly, due to various subsequent factors, forecasts, plans, goals, and other statements may not be realized as described, and actual financial results, success/failure or progress of development, and other projections may differ materially from those presented herein.

- Information concerning pharmaceuticals and other products (including those under development) contained herein is not intended as advertising or as medical advice.

Accelerating Growth Trend

Emphasizing the intrinsic values of products

Reach “patients who can be saved”” with this medicine

- Expand outreach to new patient segments to enhance healthcare impact and accelerate market share growth

Promotion based on “scientific evidence”

- Communicate economic benefits in addition to product value (safety and efficacy)

ORGOVYX®

- While expanding revenue rapidly following healthcare system reform in the U.S., retaining significant potential for further market share growth

- Aiming to reach revenue of approx. 250 billion yen in the 2030s through proactive promotional activities

Potential for share expansion in ADT*1 market

The revised FY2025 forecast is expected at approx. 150

billion yen

(Converted at the rate of 150 yen per

USD)

The revised FY2025 forecast is expected at approx. 150

billion yen

(Converted at the rate of 150 yen per

USD)

- *1Androgen Deprivation Therapy

- *2Net product revenue basis

- *3Source: Internal calculation based on information licensed from IQVIA: NSP Volume for the period 10/1 to 10/31, 2025 reflecting estimates of real-world activity. All rights reserved.

A dual approach that engages both patients and healthcare professionals

Healthcare professionals

Patients

- *4Under Medicare Part D, the annual out-of-pocket cap has been set at $2,000 in CY2025, with no out-of-pocket costs above the cap

GEMTESA®

- Expecting continued expansion of the β3 agonist market, driven in part by the entry of generics for the competing product

- Aiming to achieve revenue of approx. 150 billion yen in the 2030s through promotional investments that highlight clinical usefulness

Potential for share expansion of the β3 agonist market

The revised FY2025 forecast is expected at approx. 90

billion yen

(Converted at the rate of 150 yen per

USD)

The revised FY2025 forecast is expected at approx. 90

billion yen

(Converted at the rate of 150 yen per

USD)

- *1Overactive bladder

- *2Net product revenue basis

- *3This is based on information licensed from IQVIA: NPA for the period 10/1 to 10/31, 2025 reflecting estimates of real-world activity. All rights reserved.

Demonstrating the True Value of R&D

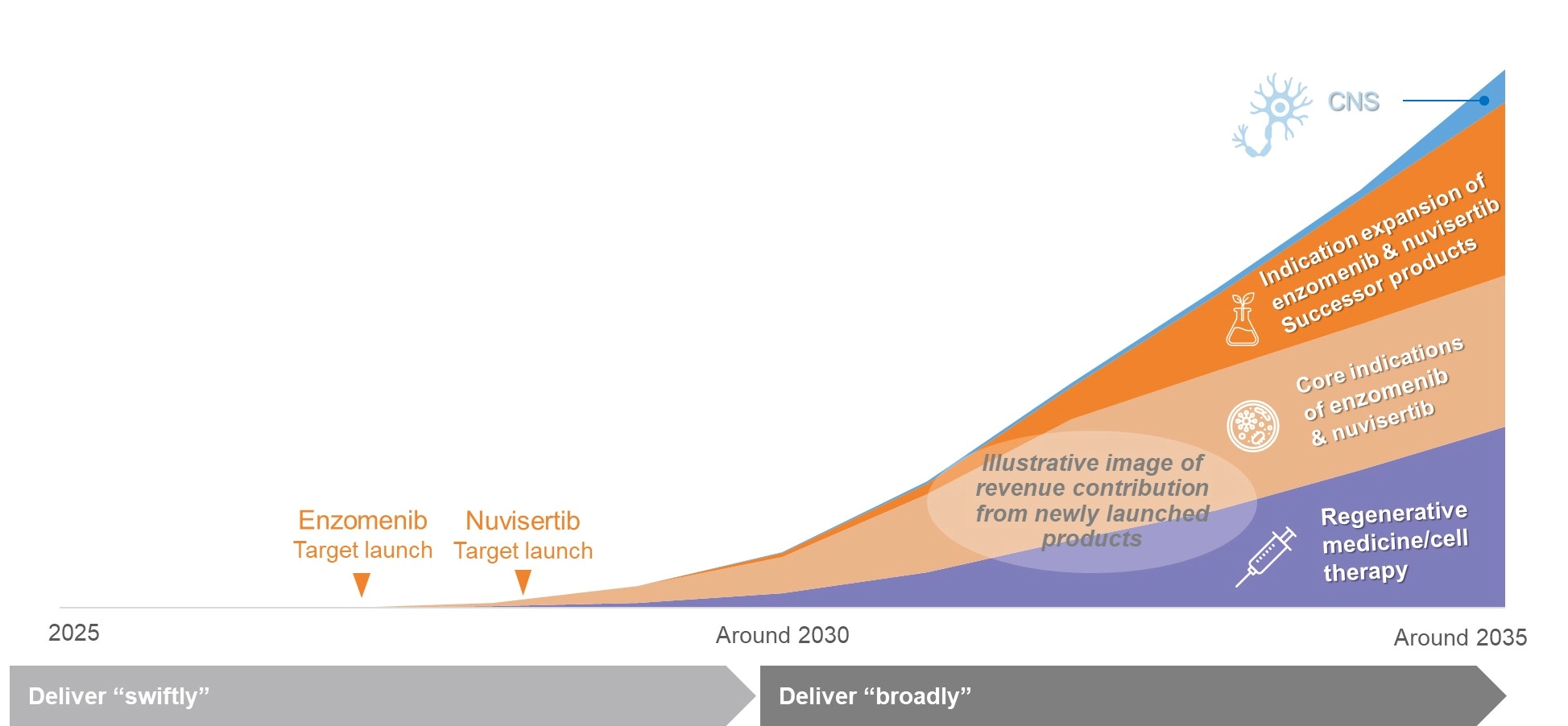

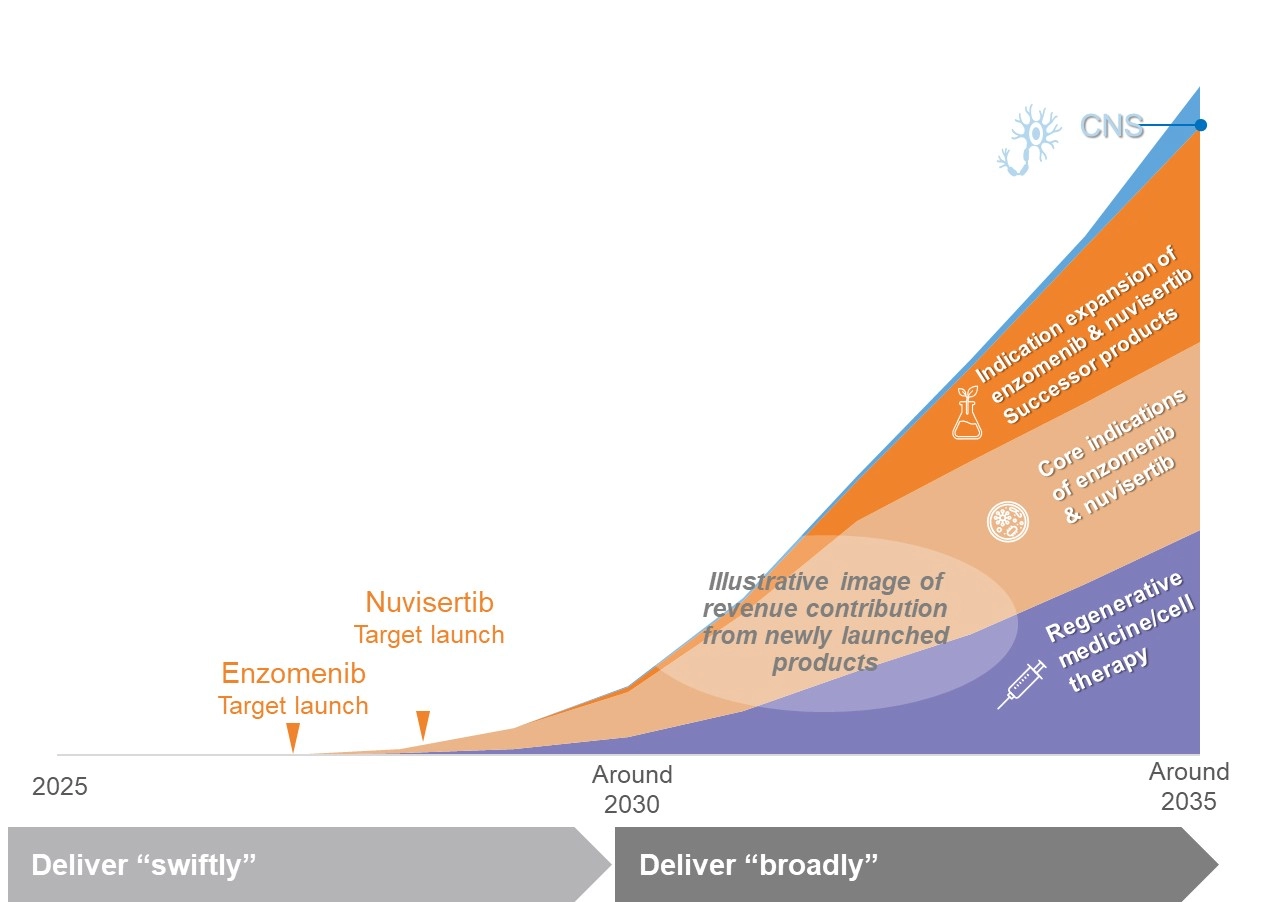

Deliver “swiftly”

- Accelerate development to deliver the most appropriate treatments to patients with acute leukemia and myelofibrosis as early as possible

Deliver “broadly”

- Advance indication expansion through the optimal approach to reach as many patients as possible

A New Revenue Stage Unlocked by the Two Oncology Compounds

- Next-generation revenue drivers following ORGOVYX® and GEMTESA®

- A touchstone for the revival of an R&D-driven pharmaceutical company through in-house innovation*

- *Received multiple regulatory designations to accelerate development from regulatory authorities in Japan, the U.S., and Europe, based on favorable drug profiles and early-phase clinical study results

- Enzomenib :Fast Track (the U.S.), Orphan drug (Japan and the U.S.)

- Nuvisertib :Fast Track (the U.S.), Orphan drug (Japan, the U.S. and Europe)

- *Received multiple regulatory designations to accelerate development from regulatory authorities in Japan, the U.S., and Europe, based on favorable drug profiles and early-phase clinical study results

- Enzomenib :Fast Track (the U.S.), Orphan drug (Japan and the U.S.)

- Nuvisertib :Fast Track (the U.S.), Orphan drug (Japan, the U.S. and Europe)

Business Potential of the Two Oncology Compounds

| Enzomenib | Nuvisertib | |

|---|---|---|

| Target Indication |

Acute leukemia

(KMT2A-rearranged or NPM 1-mutated)

|

Myelofibrosis |

| Mechanism of action | Selective menin inhibition | PIM1 kinase inhibition (novel mechanism of action) |

| Expected competitive advantages |

Promising efficacy and a favorable safety profile

(potentially lower risk of cardiac adverse events and

differentiation syndrome)

|

Promising efficacy and a favorable safety profile

(potential to improve bone marrow fibrosis)

|

| Aimed positioning |

Best-in-class therapy in the

menin inhibitor market

(No limitations on concomitant use with azole

antifungals)

|

First-in-class therapy for

first-line use in combination with the standard of care

(No limitations on use in patients with low platelet

counts)

|

| Development Phases |

Phase 1/2

Monotherapy for relapsed/refractory acute leukemia

Combination therapy with venetoclax/azacitidine for newly diagnosed |

Phase 1/2

Monotherapy for relapsed/refractory myelofibrosis

Combination therapy with momelotinib for newly diagnosed or relapsed/refractory |

| Target launch date | FY2027 | FY2028 |

| Peak sales forecast |

・ Over

100 billion yen ・ Expect over 200 billion yen with indication expansions |

・ Over

100 billion yen ・ Indication expansions under consideration |

|

|

| Enzomenib | |

|---|---|

| Target Indication |

Acute leukemia

(KMT2A-rearranged or NPM 1-mutated)

|

| Mechanism of action | Selective menin inhibition |

| Expected competitive advantages |

Promising efficacy and a favorable safety profile

(potentially lower risk of cardiac adverse events and

differentiation syndrome)

|

| Aimed positioning |

Best-in-class therapy in the

menin inhibitor market

(No limitations on concomitant use with azole

antifungals)

|

| Development Phases |

Phase 1/2

Monotherapy for relapsed/refractory acute leukemia

Combination therapy with venetoclax/azacitidine for newly diagnosed |

| Target launch date | FY2027 |

| Peak sales forecast |

・ Over

100 billion yen ・ Expect over 200 billion yen with indication expansions |

|

|

| Nuvisertib | |

|---|---|

| Target Indication | Myelofibrosis |

| Mechanism of action | PIM1 kinase inhibition (novel mechanism of action) |

| Expected competitive advantages |

Promising efficacy and a favorable safety profile

(potential to improve bone marrow fibrosis)

|

| Aimed positioning |

First-in-class therapy for

first-line use in combination with the standard of care

(No limitations on use in patients with low platelet

counts)

|

| Development Phases |

Phase 1/2

Monotherapy for relapsed/refractory myelofibrosis

Combination therapy with momelotinib for newly diagnosed or relapsed/refractory |

| Target launch date | FY2028 |

| Peak sales forecast |

・ Over

100 billion yen ・ Indication expansions under consideration |

|

|

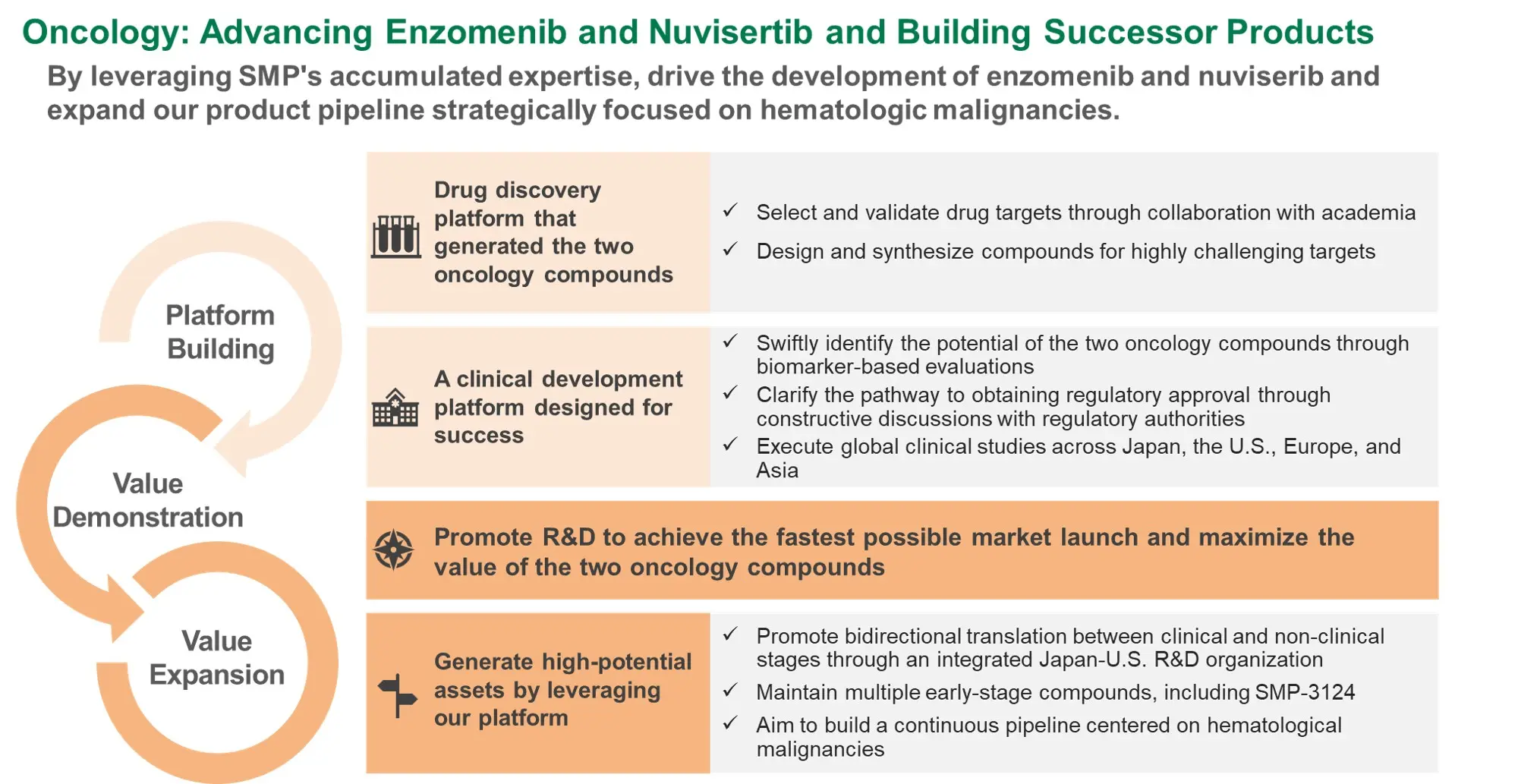

Development Strategy for the Two Oncology Compounds

- Based on the clinical potential of the two oncology compounds, focusing resources on these programs as top-priorities and pursuing the fastest possible market launch

- Determining the optimal development strategy at the next VIP* for maximizing value through indication expansions

Select and validate drug targets by leveraging the cutting-edge science and the collaboration with academia

Assess the proof-of-concept (efficacy and safety) in the early stages of clinical development by using objective indicators

At the next VIP, determine the development strategy to secure resources for indication expansions and effectively manage R&D expenses, having partnering as a primary option

Clarify the pathway to regulatory approval through constructive discussions with regulatory authorities

Identifying partners capable of appropriately evaluating the two compounds and contributing to maximizing their value

Expand clinical study sites to Europe and Asia in addition to Japan and the U.S., and drive global clinical studies forward in the highly competitive field of oncology

- *Assumed next VIPs

- Enzomenib

- Ph2 topline results in relapsed/refractory acute leukemia with KMT2A rearrangement

- Nuvisertib

- Successful Health Authority meetings on the Ph3 study design, based on results from the Ph1/2 momelotinib combination study in myelofibrosis

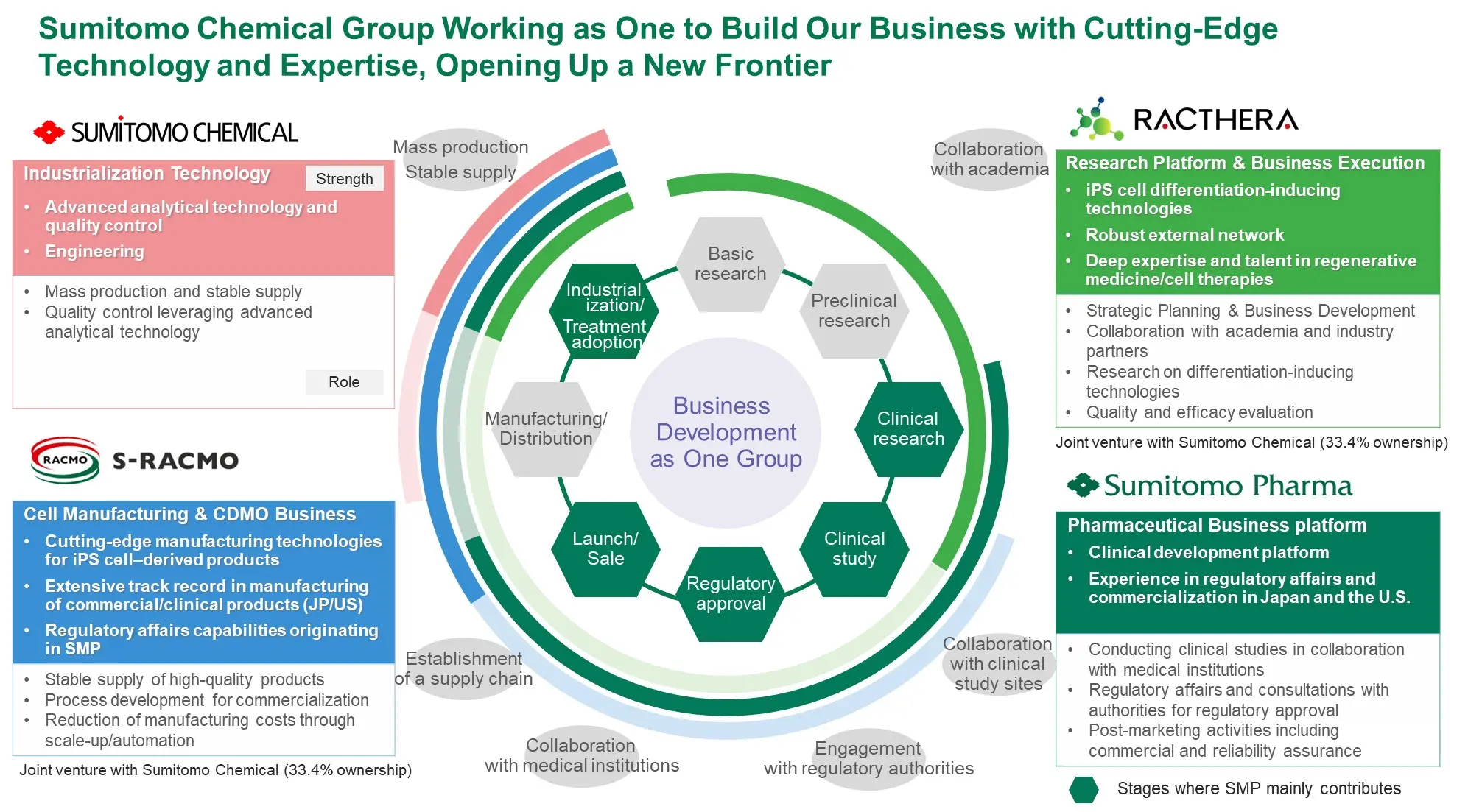

Developing and Establishing Future Growth Engines

Create value “successively”

- Leverage our technologies and expertise to build a continuously advancing, sustainable portfolio

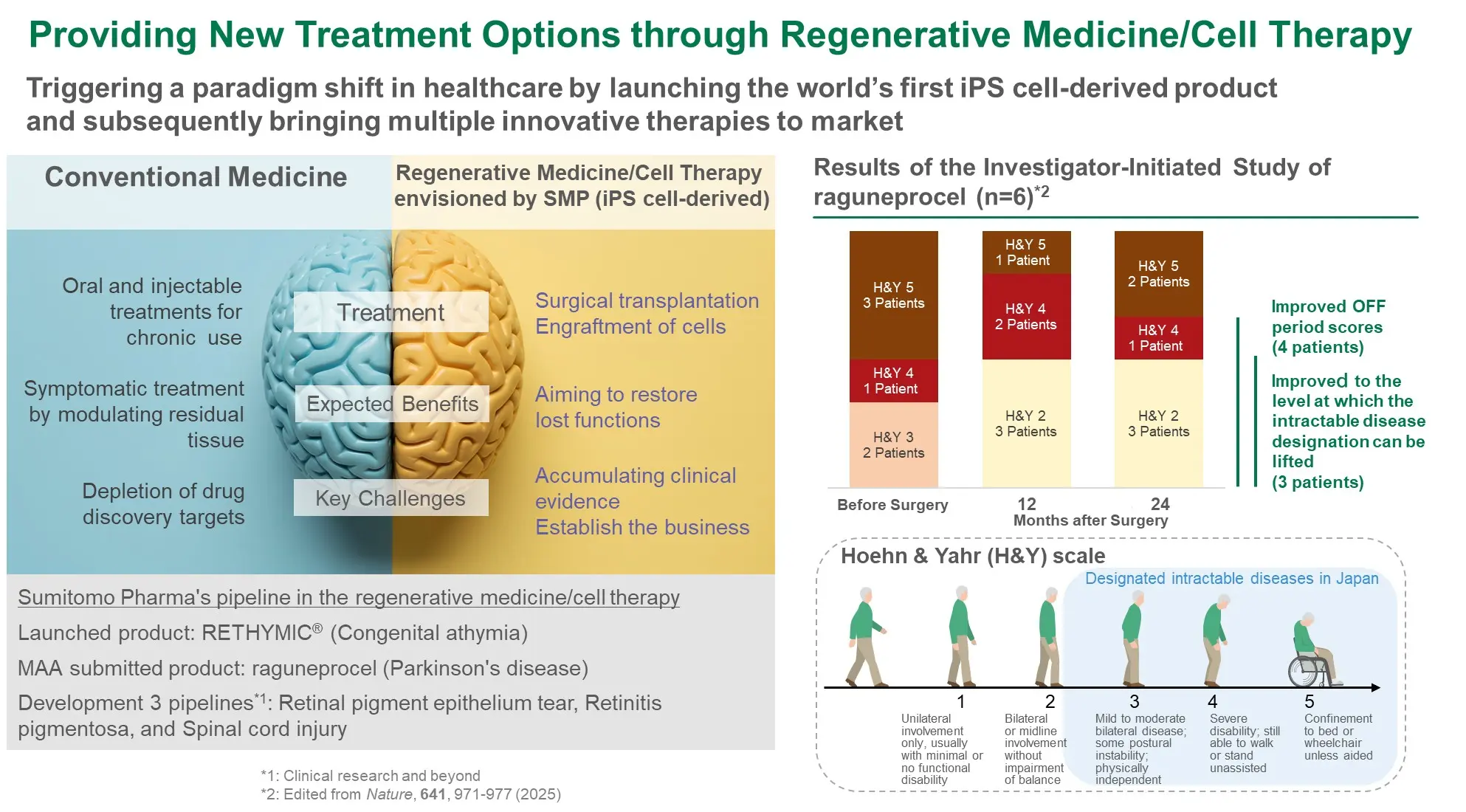

Catalyze a “paradigm shift” in healthcare

- Provide new treatment options through regenerative medicine/cell therapy

R&D Overview: Sumitomo Pharma's Value Creation Approach

- Focusing on hematological malignancies and neurodegenerative diseases (including rare neurological diseases) with high unmet medical needs where Sumitomo Pharma can leverage its strengths

- Aiming to continuously create breakthrough therapies by pursuing a development strategy that emphasizes early acquisition of objective efficacy signals in patients

Modalities where SMP Has Strength

Priority Areas for SMP’s Strategic Focus

hematological malignancies

Neuro-degenerative diseases*

- *Including rare neurological diseases

- Oncology Early‑stage clinical development data substantiating the potential of the two oncology compounds

- Regenerative Medicine : Application for regulatory approval based on clinical study results from a limited number of patients

- CNS : Advance programs while validating efficacy signals in a limited number of patients

-

Build a continuous product pipeline

Leverage the R&D platforms established in oncology

and CNS

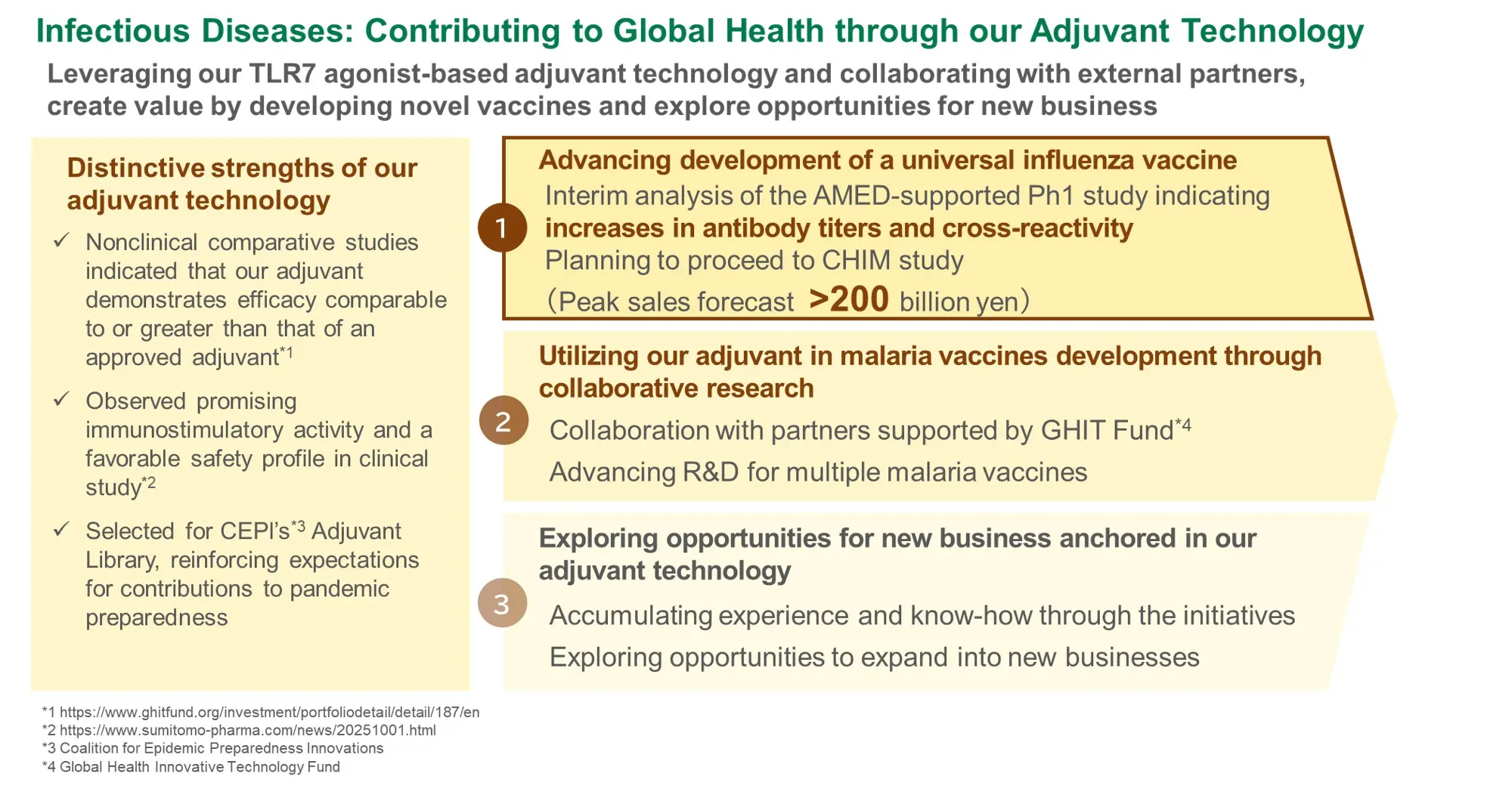

Develop vaccines and adjuvants as a new business area

Pursue stepwise validation of compound potential by leveraging cutting edge science and ensure successful progression toward regulatory approval

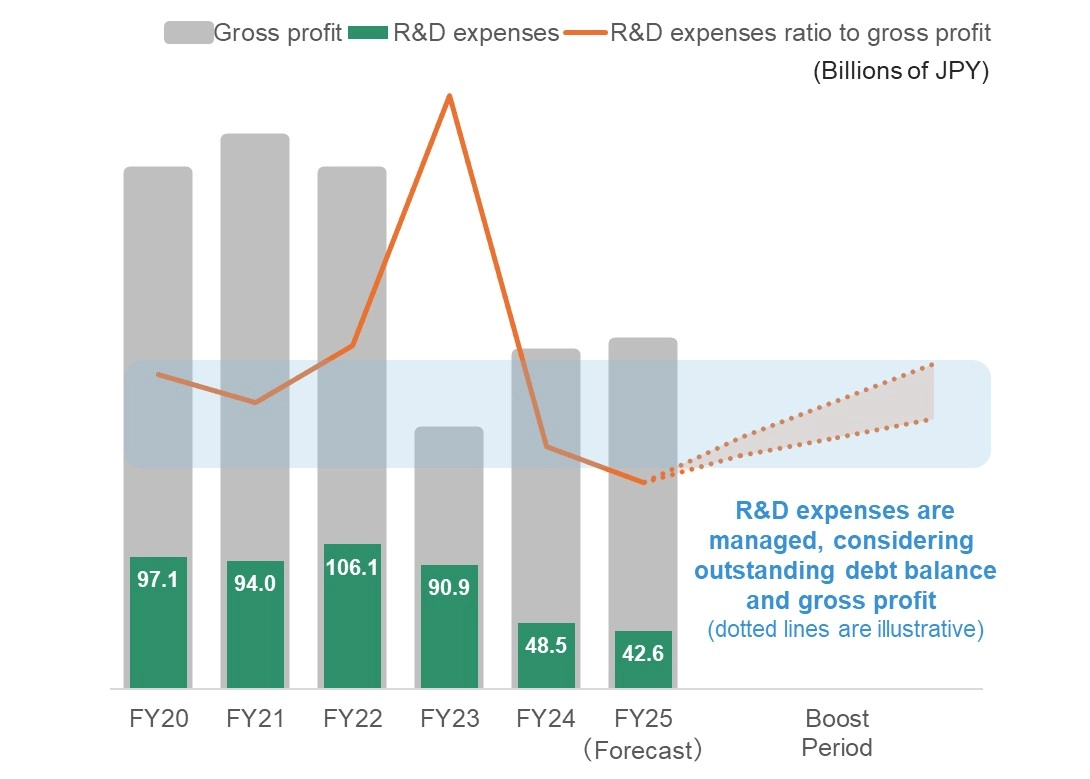

PL Management and Financial KPIs

PL Management

- While maintaining disciplined cost management with a firm commitment to securing bottom-line profits, directing investments, primarily in R&D, toward developing and establishing future growth engines

Before (FY2024-FY2025)

Emergency response to severe management challenges, with PL management driven by fundamental structural reforms

- Significant cost and workforce reduction, alongside business restructuring and divestments

- Cap‑based management of R&D expenses

- Selection and concentration of R&D programs

After

Make necessary growth investments on the premise of securing bottom-line profits and strengthening the financial base

- Maximizing revenue of ORGOVYX® and GEMTESA®

- Fastest possible market launch and expanding value of the two oncology compounds

- Developing the next-generation revenue base

Capital Allocation Policy

- Execution of medium‑ to long‑term growth investments under disciplined financial management

- Acceleration of financial‑base strengthening and next‑generation revenue foundations through external fund‑raising

NOPAT

before deduction of R&D expenses

External

fund-raising

Uses(FY2026-FY2028 total)

Investments

Capital expenditures

Investments and loans

Approx. 50billion yen

R&D expenses

Approx. 180billion yen

Repayment

Term loan Subordinated bonds (FY2027)

Approx. 200billion yen

Returns

Dividend

ー

- Aiming to resume dividends as soon as possible

- Fastest possible market launch and maximizing value of the two oncology compounds

- Developing the next-generation revenue base (CNS and infectious diseases)

- Gradually accelerating growth investments under disciplined cost control

- Strengthening existing businesses (production, quality control systems, etc.)

- Expansion of the regenerative medicine/cell therapy business through investments and loans to RACTHERA and S-RACMO

- Strategic investments expected to focus on in-licensing opportunities in Japan

- Repaying interest-bearing debt to strengthen the financial base and enhance business agility

- Utilizing other funds raised for growth investments

Financial KPIs

Reboot 2027 (FY2025-FY2027 Targets)

Targets by FY2027

As early as possible

Boost 2028 (FY2026-FY2028)

KPI Targets

Over 350 billion yen in FY2028

FY2026-FY2028

at an early stage Recover to positive net cash

Including Regenerative medicine/cell therapy business (Equity-method affiliate)

cumulatively from FY2026 to FY2028 while considering ROE

Governance Transformation

- Focusing on the balance between the value creation for growth and financial discipline, proactively strengthen governance led by the Board of Directors

Launch in Jun. 2024

New Management Team

- Monitoring fundamental structural reforms

- Strengthening awareness of PL and financial discipline

Transition in Jun. 2025

Company with an Audit & Supervisory Committee

- Improving the effectiveness of supervisory functions

- Incorporating supervisory and audit perspectives into management processes, enabling multi‑faceted discussions and decision‑making

- With a view to enabling faster decision making

Enhancing strategic discussion for the medium- to long-term

- Monitoring progress of Reboot 2027

- Discussing fundamental R&D strategy

Transitioning from “Value Creation” to “Value Delivery”

Boost

- At the Board of Directors:

- Driving comprehensive discussions on growth strategy to further enhance corporate value

- Simultaneously, prioritizing robust financial discipline to ensure the feasibility of fundamental structural reforms

Position we aspire to establish by 2033Position we aspire to establish by 2033

Global Specialized Player

Establish position as

a Global Specialized Player (GSP)

Continue to create and implement innovations in society by

strongly turning the Value Creation Cycle in specific fields

and technologies.

Establish the “Sumitomo Pharma” brand worldwide by

contributing to healthy and fulfilling lives